Ever wonder how accountants and bookkeepers know whether the numbers they report on a balance sheet are actually correct? What if a transaction was forgotten, or worse, recorded twice?

Believe it or not, this is very common, even among experienced professionals. People make mistakes, and accounting errors happen all the time. The difference is that skilled professionals don’t ignore this reality. They actively work to detect and correct errors using a variety of financial controls.

One of the most important (and powerful) of these controls is reconciliation.

What Is Reconciliation?

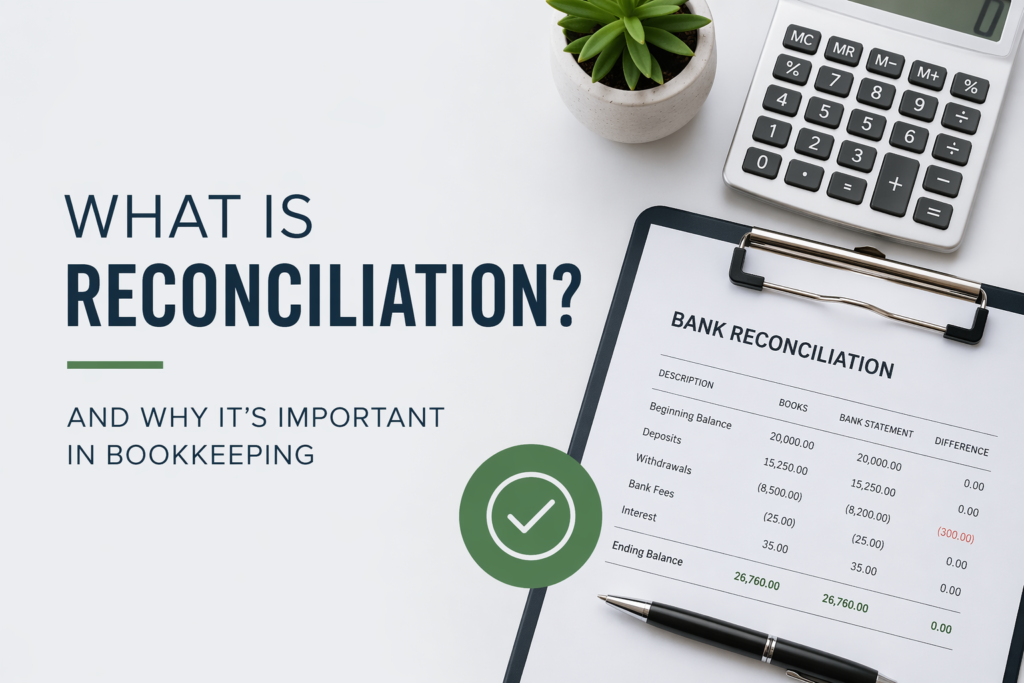

Reconciliation is the process of verifying that the amounts recorded in your financial records match an independent, objective source of truth.

For example, if your balance sheet shows a bank balance of $20,000 at the end of the month, your bank statement should show exactly the same amount on that same date. If it doesn’t, something is off, and reconciliation helps you find out why.

When a discrepancy is identified, a bookkeeper or accountant will:

- Review each transaction in the accounting records

- Cross-reference those transactions with external documents (like bank or credit card statements)

- Identify missing, duplicated, or incorrectly recorded entries

Why Reconciliation Matters

Reconciliation isn’t just a routine task; it’s essential for ensuring the accuracy and reliability of your financial data.

Even small errors can have significant consequences if left undetected. Consider this common example:

A business pays for vehicle repairs and records the transaction. However, instead of posting the cost to a repairs expense account, it is mistakenly recorded in a vehicle asset account. Since no new vehicles were purchased during the year, the bookkeeper assumes there’s nothing to review and skips reconciling that account.

The result?

- Assets are overstated

- Expenses are understated

- Profit appears higher than it actually is

Without reconciliation, this error could go unnoticed, and decisions could be made based on inaccurate financial information.

Best Practices for Reconciliation

To maintain accurate financial records, reconciliation should be performed:

- Regularly (monthly is standard, but more frequently for high-volume accounts)

- For all balance sheet accounts, not just bank accounts

- Even when there appears to be no activity

Consistency is key. Reconciliation is not just about catching errors; it’s about building confidence in your financial reporting.

The Bottom Line

Reconciliation is one of the most important safeguards in bookkeeping. It ensures that your financial statements reflect reality, not assumptions or unnoticed mistakes.

If you want to trust your numbers and make informed business decisions, you can’t afford to skip this step.

Ready for Clarity You Can Count On?

If you’re not completely confident in your numbers, it may be time to take a closer look. Accurate financial statements aren’t just about compliance and avoiding penalties; they’re the foundation for smart, informed decision-making.

Wondering whether your financial statements are truly accurate? Contact us today for a free consultation and let us help you gain the clarity and peace of mind you deserve.