Did you know that incorrectly recording an asset purchase as an expense could lead to inaccurate financial statements, tax filing errors, and costly problems if you’re ever audited? It’s one of the most common bookkeeping mistakes small businesses make, and one that’s surprisingly easy to avoid.

Disclaimer: This information is provided for educational purposes only and should not be considered tax advice. Always consult a qualified accounting professional to ensure you receive advice tailored to your specific business circumstances.

When your business purchases equipment, vehicles, computers, or other long-term assets, it can be tempting to record the entire purchase as an expense right away. After all, cash left your bank account, so it must be an expense… right?

Not quite.

While most ordinary business expenses can be fully deducted in the year they are incurred, capital asset purchases are treated differently for both accounting and tax purposes.

What Is a Capital Asset?

A capital asset is generally a significant purchase that will provide value to your business over multiple years. Common examples include:

- Computers and servers

- Office furniture

- Vehicles

- Machinery and equipment

- Buildings

- Certain software

Instead of being recorded as an expense immediately, these purchases are initially recorded on your balance sheet as assets.

How Asset Purchases Are Deducted

For accounting purposes, businesses typically recognize the cost of an asset gradually over its useful life through depreciation.

For Canadian income tax purposes, the deduction is usually claimed through Capital Cost Allowance (CCA), which follows rules established by the Canada Revenue Agency.

Although depreciation and CCA serve similar purposes, they are not always calculated the same way. Financial statement depreciation often differs from the CCA claimed on your tax return.

Why Misclassifying Assets Is Dangerous

Recording an asset purchase as an expense can create several problems:

1. Overstated Expenses

Your profit may appear lower than it actually is, which can distort management decisions and financial reporting.

2. Incorrect Tax Filings

Claiming a full deduction when only CCA is permitted could result in reassessments, interest, and penalties if discovered by the CRA.

3. Inaccurate Balance Sheet

Your financial statements may understate the assets your business owns, making your company appear less valuable than it truly is.

4. Poor Decision-Making

Accurate records are essential for budgeting, financing, and evaluating business performance.

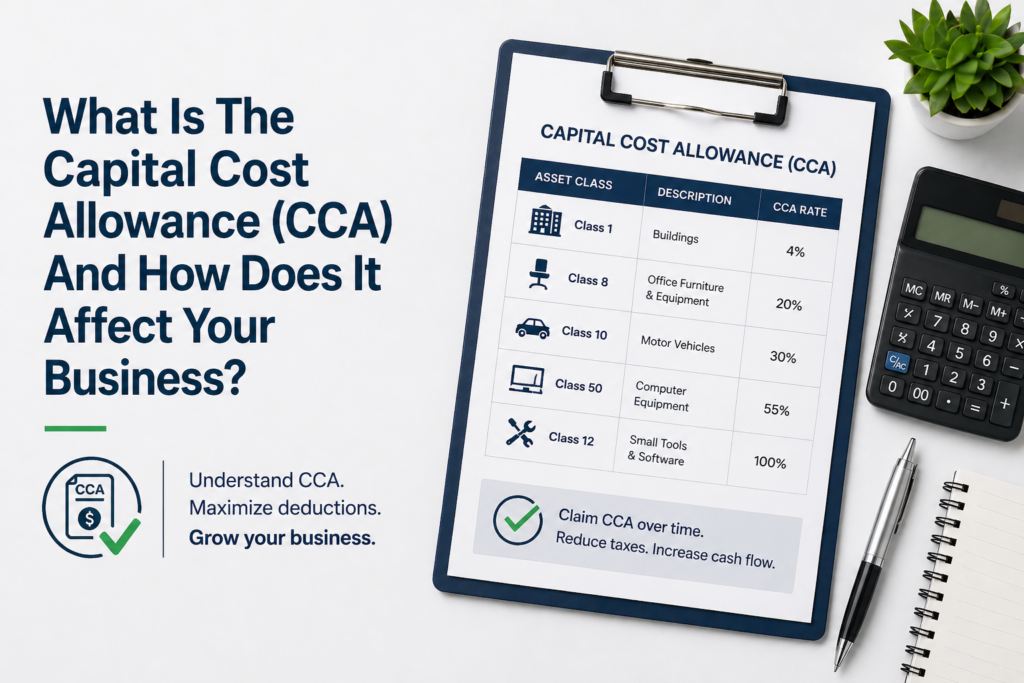

Common CCA Classes in Canada

The CRA groups capital assets into classes, each with its own prescribed depreciation rate.

Some common examples include:

| Class (Rate) | Description |

|---|---|

| Class 1 (4%) | Most buildings |

| Class 8 (20%) | Furniture, fixtures, and general office equipment |

| Class 10 (30%) | Motor vehicles |

| Class 10.1 (30%) | Passenger vehicles above the annual prescribed cost limit |

| Class 12 (100%) | Small tools costing less than the prescribed threshold and certain software |

| Class 50 (55%) | Computer hardware and systems software |

The applicable CCA rate is generally applied to the asset’s Undepreciated Capital Cost (UCC) rather than the original purchase price.

Understanding the Half-Year Rule

In most cases, only half of an asset’s net additions are eligible for CCA in the year of acquisition. This is known as the half-year rule.

For example, if your business purchases some computer hardware for $5,000 in Class 50:

- Cost: $5,000

- Eligible amount in Year 1: $2,500

- CCA rate: 55%

- First-year CCA claim: $1,375

The remaining balance becomes part of your UCC pool for future years.

How to Avoid This Mistake

To prevent costly errors:

- Review large purchases carefully before recording them.

- Establish capitalization policies for your business.

- Use accounting software that properly tracks fixed assets.

- Consult your bookkeeper or accountant when uncertain.

When in doubt, it’s always better to ask first than amend later.

Final Thoughts

Misclassifying asset purchases as expenses is a small bookkeeping error that can create significant tax and financial consequences.

Properly recording capital assets helps ensure accurate financial statements, compliance with CRA rules, and better long-term decision-making.

If you’re unsure whether a purchase should be expensed or capitalized, professional guidance can save you time, money, and stress.

Need Help Reviewing Your Books?

Proper asset classification is essential for accurate financial reporting and tax compliance.

Book a free consultation today to receive a professional review of your bookkeeping and personalized recommendations for your business.